Australia Economic Progress Report

Current Events

A significant event from the perspective of domestic Australian economy is the minutes of the latest Monetary Policy Committee released on March 2019. About an year ago, the RBA was looking to increase the cash rate but the persistent economic conditions (both domestic and global) have not allowed for the same as status quo has been maintained. In the recent minutes, the slowdown in China has been addressed coupled with deterioration in the leading indicators related to unemployment (RBA, 2019). This is leading to a strong expectation of a rate cut of 25 bps in the current year by RBA.

The cash rate is significant since it would impact the interest rate which would in turn impact various macroeconomic variables indicated below (Mankiw, 2016).

- Aggregate demand would increase owing to lowering of interest rates by banks.

- This would potentially lead to higher inflation coupled with higher GDP growth in the medium term.

- Additionally, on account of higher consuming spending, it is expected that private investment cycle would be kicked off.

- Also, there would be a depreciation in the currency as money might move from the debt funds owing to better interest rates being offered elsewhere.

- The credit growth may improve along with providing much needed support to the real estate market which is the verge of collapsing especially as China enters a slowdown.

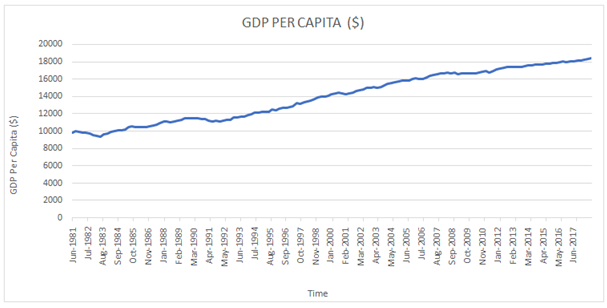

GDP Highlights

The requisite excel chart indicating GDP per capita from June 1981 to June 2018 is illustrated as follows.

The two consumption categories which witnessed the largest growth rate over the most recent quarter are transport services and insurance & other financial services.

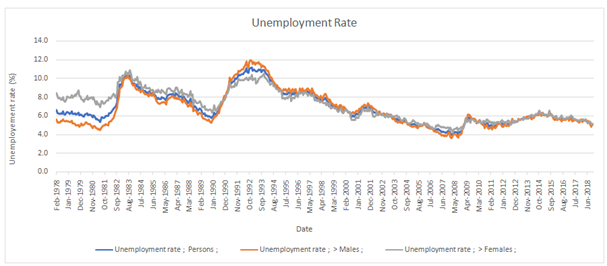

Labour Market Highlights

The requisite excel chart for the comparison of overall unemployment rate with the respective unemployment rate of male and females over the entire period is illustrated as follows.

- “Community and Personal Services” is the occupation which has witnessed the most percentage change in the most recent quarter.

- The occupation category which has switched in terms of gender concentration is “Professionals”.

- The occupation category which has shown smallest difference between male and female employment over the entire period is “Professionals”.

- The requisite occupation category which has a higher proportion of female employment over the entire period is “Clerical and Administrative Workers”.

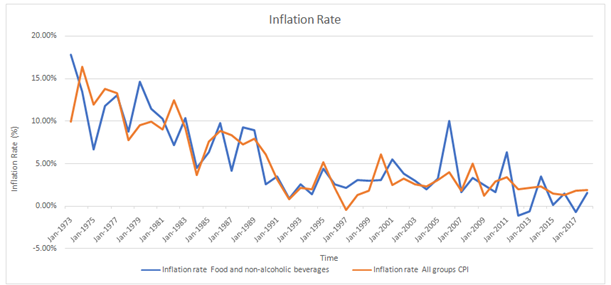

Price Movements

The requisite inflation rate graph for the entire period is shown below.

The greatest variability in the inflation rate in the 1990’s has been witnessed for Housing.

Risk Outlook

The current global environment is filled with uncertainties on multiple fronts. However, one risk that is overwhelming is the economic slowdown in China. The manufacturing sector has also shown signs of slowing down which is expected to have a ripple effect globally considering that China is the second largest economy in the world (Irvine, 2019)

China’s economy is of great interest to Australia because of the following reasons (Chau, 2019).

- Almost one third of Australia’s exports are to China. Any slowdown in China would imply that the demand for these imports from Australia would reduce.

- With regards to composition of exports from Australia, 30 % is attributed to coal and iron ore which amount to $ 120 billion annually. Considering that China is the largest consumer of coal and iron ore in the world, hence slowdown in China would impact the commodity prices driving the exports lower.

- The exports of services could also be adversely impacted considering that $32.4 billion worth of earnings from international students. A sizable chunk of these are from China.

- Also, the tourism industry would be adversely impacted considering that last year, Chinese tourists spent $ 11.3 billion in Australia.

- The real estate market may also face adverse price movements owing to the significant investments by Chinese nationals in Australia housing and commercial estate market especially in Sydney and Australia.

- Owing to falling trade, there would a increase in the budget deficit which would cause depreciation of AUD besides requiring cut on government expenditure. This would lead to lowering of GDP growth at a time when the Australian economy is in a difficult phase (Irvine, 2019).

References

Chau, D. (2019) Australia’s fortunes are linked to China’s economy — for better or worse, [online] Available at https://www.abc.net.au/news/2019-01-15/china-economy-slowdown-will-affect-australia/10716240 [Accessed on March 26, 2019]

Irvine, J. (2019) What will a China slowdown mean for the Australian economy?, [online] Available at https://www.smh.com.au/business/the-economy/what-will-a-china-slowdown-mean-for-the-australian-economy-20190125-p50tlx.html [Accessed on March 26, 2019]

Mankiw, G. (2016). Principles of Macroeconomics (6th ed.). London: Cengage Learning, pp. 65-67

RBA (2019) Minutes of the Monetary Policy Meeting of the Reserve Bank Board, [online] Available at https://www.rba.gov.au/monetary-policy/rba-board-minutes/2019/2019-03-05.html [Accessed on March 26, 2019]