Algorithm

IN Stock price S of the underlying time T-exercise price K, risk free interest rate r,

Current dividend q.

Implied Volatility

Cumulative normal distribution N ().

Step 0

Step 1

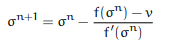

Compute n value 0 to N-1

OUT N is approximate value for the implied volatility imp (k, t).