Background:

With the objective of tweaking unhealthy conduct and food habits in Jersey City, New Jersey, the mayor of the city Steven Fulop has ensured that sale of soda is prohibited in the second most populous city of in the US. The cost benefit analysis of the decision of the decision of banning soda in the city is conducted here to evaluate whether the benefits of banning soda in the city have exceeded the cost the decision or not.

Stakeholder analysis: Identification of cost and benefits associated with soda ban

Along with ban of soda other sugary drinks have also been banned in the Jersey City meaning that people in the city will not be able to buy soda and any other sugary drinks. More than 30% of the adults in Jersey City are obese with high rate of child obesity also observed in the City. In fact the entire state of New Jersey has banned sale of Soda in schools all across the state to control child obesity. Thus, the associated benefits in the form of improved health of children and adults in the city are huge. The cost associated with ban of soda sale include tax on sale of soda paid by the producers and retailers, loss of production affecting GDP and reduction in real wage. The summary of cost and benefits along with respective stakeholders is provided in the table below:

| Costs (stakeholder) | Benefits (stakeholder) |

| Reduction in tax paid by the producers and retailers of soda (Government) | Improve quality of health (Citizens / Government) |

| Decline in GDP (Government) | Increase in sale of juice and healthy soft drinks (Government /Citizens) |

| Decline in real wage (Citizens) | Reduction in obesity leading to reduction in medical costs (Citizens) |

Assigning monetary value to the cost and benefits of soda ban:

Assigning monetary value to the cost of the decision of banning soda sale in Jersey City on the basis of best possible judgment:

| Average annual consumption of Soda in Jersey City (Number of containers) | 4,134,000 |

| Average cost per container ($) | 1.99 |

| Average annual revenue ($) | 8,226,660.00 |

| Tax included @18% | 1,254,914.24 |

| Expected decline in real wage (20% of gross revenue forgone) | 1,645,332.00 |

Thus, the GDP of the country will be reduced by approximately $8.30 million, i.e. $8,226,660 to be exact with the decision of banning sale of soda in the city. This based on the assumption that out of total population of approximately 265,000, 30% of the population consumes soda at least once a week with average container of a soda priced at $1.99 each.

Considering a standard tax rate of 18% is applicable of soda and other sugary drinks hence, the expected decline in revenue to the government in the form of tax expected to be $1,254,914 per annum. Further with assumption of 20% average revenue used to pay wages to the workers and employees in the industry the reduction in real wage is expected to be $1,654,332 per annum.

Assigning monetary value to the benefits of the decision of banning soda sale in Jersey City on the basis of best possible judgment:

| Improve quality of health | 41,133,300.00 |

| Increase in sale of healthy soft drinks including juice | |

| Increase in GDP | 3,290,664.00 |

| Tax included in GDP | 501,965.69 |

| Increase in real wage | 658,132.80 |

| Reduction in medical costs | 16,453,320.00 |

Improvement in health of the peoples of the city though cannot be measured in terms of monetary value however, it is easily 5 time more than the loss in the amount of revenue due to ban of soda sale. The expected reduction in medical cost is expected to be $16,453,320 as the city has seen significant increase in medical cost due to increase in obesity (Rouwendal, 2019).

Observation:

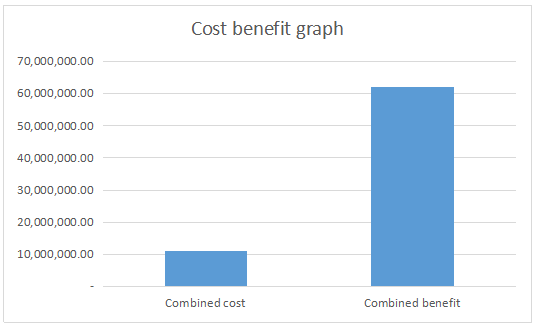

Thus, if all the monetary value of different costs are combined then the cost of the decision is $11,126,906 whereas combined benefit value expected to be $62,037,382 as can be seen from the graph below.

Thus, expected benefit of the decision is much more than the cost of banning soda sale in Jersey City. Cost benefit analysis here clearly shows that the decision of banning sale of soda in the city has far greater benefits than the cost associated with the decision (Bowden & Belfield, 2017).

References

Bowden, A., & Belfield, C. (2017). Evaluating the Talent Search TRIO program: A Benefit-Cost Analysis and Cost-Effectiveness Analysis. Journal Of Benefit-Cost Analysis, 7(4), 572-602. doi: 10.1017/bca.2015.48

Rouwendal, J. (2019). Indirect Effects in Cost-Benefit Analysis. Journal Of Benefit-Cost Analysis, 6(2), 1-27. doi: 10.1515/2152-2812.1046

| Expected number of | |

| Average annual consumption of Soda in Jersey City (Number of containers) | 4,134,000 |

| Average cost per container ($) | 1.99 |

| Average annual revenue ($) | 8,226,660.00 |

| Tax included @18% | 1,254,914.24 |

| Expected decline in real wage (20% of gross revenue forgone) | 1,645,332.00 |

| Combined cost | 11,126,906.24 |

| Improve quality of health | 41,133,300.00 |

| Increase in sale of healthy soft drinks including juice | |

| Increase in GDP | 3,290,664.00 |

| Tax included in GDP | 501,965.69 |

| Increase in real wage | 658,132.80 |

| Reduction in medical costs | 16,453,320.00 |

| Combined benefit | 62,037,382.49 |