Aim of the memo is to highlight the issues recently raised by IASB in context of goodwill and impairment. Goodwill is generally reported by the entity while it acquires any other entity and the same is reported to reflect the future profit that is expected to be generated from the assets those are acquired in the process of acquisition or merger not separately identified. Initially, in accordance with AASB 136 / IAS 36, goodwill used to be tested only for annual impairment. However, owing the users and investor’s concerns regarding the present practice IASB board is considering reintroduction of goodwill amortization in replacement of the existing approach of impairment-only. Hence, the memo will critically analyse the amortization approach as against the impairment only approach.

As per IAS 36, Para 90, goodwill acquired in the process of business combination shall be annually tested for the purpose of impairment irrespective of whether there is any warning for impairment or not and the same came into force in 2004. However prior to that period IAS 22 business combination required that the acquired goodwill shall be amortised over the useful life with the assumption that the useful life will not exceed 20 years. In case the assumption invalidates, the goodwill acquired shall be tested for the purpose of impairment at least once at the closing of each financial year regardless of whether there is any warning for impairment or not. However, different issues identified by the board in context of the same are – (i) generally it is impracticable predicting goodwill’s useful life along with the pattern in which the same reduces. Owing to the same, amortisation amount is the best possible way to describe the amount of goodwill consumption in arbitrary manner (ii) amortisation provided in straight line basis over the arbitrary useful life is not able to provide the useful information (iii) in case operational and rigorous impairment test is developed, the entity will be able to offer more useful information to the users of financial statement where amortisation of goodwill is used.

Hence, number of participants in PIR (post-implementation review) of IFRS 3 suggested reintroduction of goodwill amortisation. Different advantages in context of the same also highlighted are – (i) some of the investors were in the view that impairment-only method is useful for associating price that is paid for acquiring and for computing return on the invested capital, verifying acquisition is performing as per expectation. Further various participants felt that the losses on account of impairment are identified too late or not identified in timely manner. It was felt that the same have only confirmatory value and does not have predictive value (ii) different participants felt that procedure of impairment test is time consuming, expensive, complex and require significant judgements.

Arguments those can be placed for reintroducing the amortisation are – (i) consideration of PIR was contentious or crucial in the development phase of standard and is anticipated to recognise the areas where implementation issues or unexpected costs have been met. One of these crucial issues is amortisation (ii) decision of the board for implementing the impairment–only approach was established on conclusion that the same will offer more useful information to the financial statement users and impairment test was operational as well as rigorous. Questionable conclusion in context of the same were – (a) though some of the stakeholders feel that impairment test offer useful information, value provided by the same is confirmatory only (b) losses on account of impairment often are not reported in timely manner and it raise doubts regarding whether impairment test is rigorous (iii) feedback specified that impairment test is time consuming, expensive and complex and hence creates doubts whether it is operation to the extent it was considered by the board.

On the other hand, arguments those can be placed for retaining impairment-only approach are – (i) amortisation charge offers the financial statement users with no useful information in case the useful life is arbitrary (ii) some of the investors informed that impairment-only approach is useful for associating the price that is paid for acquiring and for computing return on the invested capital, verifying acquisition is performing as per expectation. They further mentioned that the information offered by impairment test is useful as it has confirmatory value. On the contrary, they feel that goodwill amortisation in subsequent years may provide ambiguous price that is originally paid and hence, become more difficult in analysing the stewardship. In addition, amortisation will reduce opportunity of impairment to take place. Hence, introduction of amortisation will mask the goodwill impairment along with some amortisation charges that will further reduce usefulness of information offered by impairment test. Amortisation reintroduction will lower the information quality and the same can be difficult for supporting re-introduction of amortisation of goodwill if the information is less useful.

While reviewing both the arguments question that the board was facing is not to access whether the goodwill amortisation is better approach in context of concepts for succeeding accounting for goodwill as against the approach of impairment-only. Rather question here is whether strong case is there for making changes for reintroducing goodwill amortisation approach and whether any benefits will exceed the disruption and cost that will be resulted into for changing again the requirements. However, it can be concluded that reintroducing the amortisation model will not solve the issue associated with impairment-only approach to recognise the loss in timely manner. In addition while the goodwill’s useful life is arbitrary carrying amount of goodwill acquired after deducting the charges of amortisation will not provide the original benefits from business combination that will considerably be better as compared to impairment-only approach. Hence, these facts shall be kept in mind before reintroducing the amortisation approach.

Yours’ sincerely,

John Mathew,

Accountant, Bottom Line Accounting

To,

Mr Neil Jackson

Senior Accountant, ABC Limited

Subject: – Impact of IASB’s proposed developments

Dear Mr Jackson,

Objective of preparing this letter is providing information in context of the proposed development by IASB on account of goodwill and its impact on the organisation’s profitability. I will discuss the method applied by ABC Limited for computation as well as reporting the amount of goodwill and its treatments. Mainly the letter will take into account the recent acquisition made by ABC Ltd and computation of goodwill generated on account of the same acquisition.

Based on the computation made that is attached in the appendix, it can be noticed that if the entity adopts the amortisation approach the value for amortisation over the years remain same and goodwill value is reduced by constant amount. Major reason behind adopting the amortisation approach is that the value of goodwill will kept on reducing on straight line basis year after year and at the end of the life the remaining value will become nil. In the given case, the value of goodwill is getting reduced by $ 127,500 in each year as amortization expenses. This approach is considered as effective for computing goodwill value however, the entity is not able to deliver actual value of the goodwill as the amortisation expenses is charged on the basis of the assumption that the life of goodwill is ten years and the goodwill is assumed at fixed rate in each year. However, in reality this may not be the case. Hence, number of analysts and investors raised concern that the amortisation approach shall not be used as it fails to provide exact value of the goodwill and the entire valuation is based on the assumption. In addition, high amount of amortisation expenses even in the later period of goodwill’s useful life will have an adverse impact on the profits of the entity that will in turn adversely impact the market value of the firm if it is not clearly mentioned through disclosures that the profit has been reduced owing to amortization expenses.

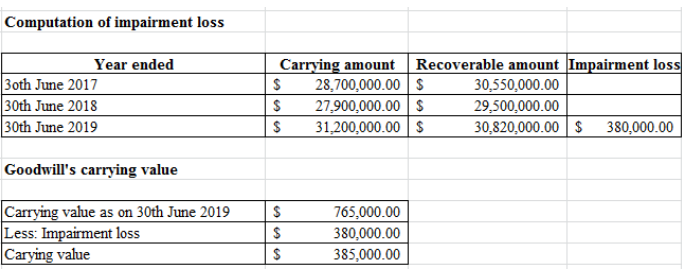

In accordance with the above presented computation it can be identified that if the entity follows the impairment-only approach the entity will not face any impairment for the year ended 30th June 2017 as well as 30th June 2018 as the recoverable amount of the goodwill is greater than the carrying amount and the impairment takes place while the carrying amount is greater than the recoverable amount of goodwill. Accordingly, for the year ended 30th June 2019 the firm will report impairment loss amounting to $ 380,000 as the carrying amount exceeds the recoverable amount by $ 380,000. This amount will be charges as an expense in the income statement of the entity for the year ended 30th June 2019 and the residual value will be reported under the balance sheet for the same period.

However, this method may be considered as complex and time consuming by the users. Hence, the amortization approach may be used after keeping in mind the facts that the goodwill’s useful life is arbitrary and carrying amount of goodwill acquired after deducting the charges of amortisation will not provide the original benefits from business combination that will considerably be better as compared to impairment-only approach.

Yours sincerely,

John Mathew,

Accountant, Bottom Line Accounting

Bibliography

Alao, A., 2017. The burden of collective goodwill: The international involvement in the Liberian civil war. Routledge.

Andersson, T., Haslam, C., Tsitsianis, N., Katechos, G. and Hoinaru, R., 2016. Stress testing International Financial Reporting Standards (IFRSs): Accounting for stability and the public good in a financialized world. Accounting, Economics and Law-a Convivium.

Ayres, D.R., Neal, T.L., Reid, L.C. and Shipman, J.E., 2019. Auditing Goodwill in the Post‐Amortization Era: Challenges for Auditors. Contemporary Accounting Research, 36(1), pp.82-107.

Chen, W., Shroff, P.K. and Zhang, I., 2017. Fair value accounting: consequences of booking market-driven goodwill impairment. Available at SSRN 2420528.

Glaum, M., Landsman, W.R. and Wyrwa, S., 2018. Goodwill impairment: The effects of public enforcement and monitoring by institutional investors. The Accounting Review, 93(6), pp.149-180.

Ifrs.org. 2019. [online] Available at: https://www.ifrs.org/-/media/feature/meetings/2019/june/iasb/ap18b-goodwill-and-impairment.pdf [Accessed 12 Oct. 2019].

Johansson, S.E., Hjelström, T. and Hellman, N., 2016. Accounting for goodwill under IFRS: A critical analysis. Journal of international accounting, auditing and taxation, 27, pp.13-25.

Kabir, H., Rahman, A. and Su, L., 2017. The Association between Goodwill Impairment Loss and Goodwill Impairment Test-Related Disclosures in Australia. In 8th Conference on Financial Markets and Corporate Governance (FMCG).

Knauer, T. and Wöhrmann, A., 2016. Market reaction to goodwill impairments. European Accounting Review, 25(3), pp.421-449.

Li, K.K. and Sloan, R.G., 2017. Has goodwill accounting gone bad?. Review of Accounting Studies, 22(2), pp.964-1003.

Mazzi, F., André, P., Dionysiou, D. and Tsalavoutas, I., 2017. Compliance with goodwill-related mandatory disclosure requirements and the cost of equity capital. Accounting and Business Research, 47(3), pp.268-312.

Schatt, A., Doukakis, L., Bessieux-Ollier, C. and Walliser, E., 2016. Do goodwill impairments by European firms provide useful information to investors?. Accounting in Europe, 13(3), pp.307-327.

| Computation of goodwill amortization | |||

| Goodwill value | $1,275,000.00 | ||

| Amortization period | 10 years | ||

| Year | Amortization value | Accumulated value of amortization | Carrying value |

| 1st July 2016 | $- | $- | $1,275,000.00 |

| 30th June 2017 | $127,500.00 | $127,500.00 | $1,147,500.00 |

| 30th June 2018 | $127,500.00 | $255,000.00 | $1,020,000.00 |

| 30th June 2019 | $127,500.00 | $382,500.00 | $892,500.00 |

| 30th June 2020 | $127,500.00 | $510,000.00 | $765,000.00 |

| 30th June 2021 | $127,500.00 | $637,500.00 | $637,500.00 |

| 30th June 2022 | $127,500.00 | $765,000.00 | $510,000.00 |

| 30th June 2023 | $127,500.00 | $892,500.00 | $382,500.00 |

| 30th June 2024 | $127,500.00 | $1,020,000.00 | $255,000.00 |

| 30th June 2025 | $127,500.00 | $1,147,500.00 | $127,500.00 |

| 30th June 2026 | $127,500.00 | $1,275,000.00 | $- |

| Computation of impairment loss | |||

| Year ended | Carrying amount | Recoverable amount | Impairment loss |

| 3oth June 2017 | $28,700,000.00 | $30,550,000.00 | |

| 30th June 2018 | $27,900,000.00 | $29,500,000.00 | |

| 30th June 2019 | $31,200,000.00 | $30,820,000.00 | $380,000.00 |

| Goodwill’s carrying value | |||

| Carrying value as on 30th June 2019 | $765,000.00 | ||

| Less: Impairment loss | $380,000.00 | ||

| Carying value | $385,000.00 |