Accounting Assignment Writing help analysis on:: Description of accounting concepts and conventions – Techniques for appraising capital projects

a)Five of the accounting concepts and conventions

Going concern concept:

The going concern concept or principle says that financial accounts should be prepared with the mindset that the business will always be in existence and will never cease its operations. All the financial & accounting disclosures should be made with the mindset that the business is a going concern (Khan, M.Y. ,1993).

The going concern principle also requires that if those preparing the financial statements have any doubts regarding the future survival and viability of the company then they should disclose their doubts and misgivings about the future status of the company in full detail.

Take for example that Christopher NATO Limited has too much debt on its balance sheet. This debt poses a threat to the going concern status of the company. So going by the going concern concept and accounting best practices it would be appropriate to clearly state in the financial statements of the company that the debt may pose a threat to the future survival of the company. These disclosures should be mentioned in the notes to the financial statements.

The business will never be liquidated and hence will be a going concern is the assumption of the going concern concept. The business will be operational at least in the foreseeable future(Khan, M.Y. ,1993).

Business Entity Concept:

Another important accounting concept is the business entity concept. The owner and the business are two separate entities in the eyes of accounting. A layman often confuses the owner and the business to be the same. This is not the case according to the business entity concept.

A business or company has a separate legal status from its promoters and owners. So Christopher NATO limited has a separate legal and contractual status from its promoters or shareholders.

The business stands apart as a distinct business and economic entity. The transactions of the business are recorded separately from its owners’ personal transactions. This separate recording of the transactions of the owner and business enables clear determination of the true financial position of the business(Khan, M.Y. ,1993).

Principle of Conservatism:

Principle of Conservatism is an important accounting concept. It says that .conservatism should be adhered to when assessing the assets or income of a business entity. So if there are two methods for assessing the value of the assets of Christopher NATO limited then the one which assigns a lower value to the assets should be given preference over the one that assigns a higher value to the assets.

Accountants should avoid overstating the expected income or value of the assets of a business entity. At the same time, in case of calculation of expected or probable losses that method should be chosen which gives the maximum possible losses (Nitzan, Jonathan; Bichler, Shimshon ,2009).

Window-dressing is the practice of using creative accounting to inflate the value of assets or profits of a company. Companies when resorting to this unethical practice often flout the principle of conservatism.

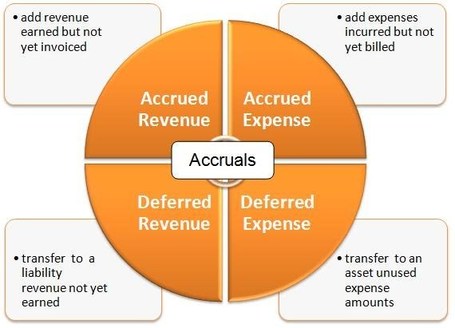

Accrual principle of accounting:

The accrual principle of accounting says that revenues should be recorded in the accounts as soon as they are accrued or realized instead when actual cash is realized. So if, for example, Christopher NATO limited makes a credit sale of $ 100000 in January. The financial year ends on March 31st , March 2012. The cash of this credit sale is likely to be received in June 2012. Then according to accrual principle of accounting the sale should be recorded as an accrued revenue asset in the balance sheet of financial year 2011-12 even if the actual cash for this sale will be received in financial year 2012-13(Nitzan, Jonathan; Bichler, Shimshon ,2009).

Revenue recognition principle is a very important one in accounting. Revenue is said to be recognized as soon as the invoice of the sale is accepted by the customer. The customer may choose to pay immediately on receiving the invoice of sale or it may choose at a latter point of time. In some cases he may even pay in advance i.e. before the actual sale has taken place. In these cases the revenue will be recognized as deferred revenue. Deferred revenue is a liability for the business.

Double Entry Accounting System:

The double entry accounting system means that every financial or accounting transaction affects two accounts in the accounting books of the business. One of these accounts should be debited while the other should be credited.

If the account is that of an asset then it is debited in case of increase in assets and is credited in case of decrease in assets. If the account is a liability one then it is credited in case of increase in liabilities and is debited in case of decrease in liabilities.

If the account is an income or revenue account then it is credited in case of increase in income or revenue and is debited in case of decrease in income or revenue. If it is an expense account then it is debited in case of increase in expenses and is credited in case of decrease in expenses. A capital or equity account is credited in case of increase in capital and is debited in case of decrease in capital (Revsine, Lawrence,2002).

b) Two categories of techniques used for appraising capital projects:

Capital projects are those projects which are expected to generate revenue for a company in future. While making investment decisions it is important that a company appraises the various alternative capital projects that it can choose from.

Appraisal of capital projects is a very important activity for the finance team of any business because it has strategic, long term implications. Two of the widely used categories for appraising capital projects are discounted cash flow methods (NPV and IRR) and payback period methods (Weygandt, Jerry J,2009).

Payback period method for capital appraisal:

In the payback period method the project having a shorter payback period is chosen over the one having a longer payback period. Suppose, for example, Christopher NATO limited has to choose from two projects, A and B.

Project A requires an initial investment of $ 100000. It is likely to generate $ 10,000 annually over the next fifteen years. Then the payback period for this project will be:

$ 100000 / $ 10000 = 10 years

Project B requires an initial investment of $ 200000. It is likely to generate $ 15,000 annually over the next fifteen years. Then the payback period for this project is:

$ 200000 / $ 15000 = 13.33 years.

According to this capital appraisal technique, project A has a shorter payback period than project B. Therefore project A should be chosen over project B.

Payback period is not a very good technique for capital appraisal. It does not take into account the time value of money. It treats $ 100 received today as equal to $ 100 received a year or two hence. This is a very serious flaw of this method.

The discounted payback period method tries to overcome this limitation. It discounts future cash flows by a suitable discount rate. This discount rate is usually the weighted average cost of capital (Pieters, A. Dempsey, H. N ,2009).

Discounted cash flow techniques:

Net present value method:

In net present value method the present value of future cash flows is subtracted from the present value of cash outflows to calculate the net present value (NPV) of the capital project. If the NPV is greater than zero then the project is accepted and if the NPV is less than zero then the project is considered to be a loss making one.

In case of two or more competing projects, the project having the highest NPV is accepted. The present value of cash flows is calculated by discounting the future cash flows with a suitable discount rate. The discount rate is usually taken equal to the weighted average cost of capital (WACC).

The WACC is calculated as :

WACC = Debt / (Debt + Equity) * After tax cost of debt + Equity / (Debt + Equity )

Suppose for example Christopher NATO limited wants to appraise a project A which requires an initial investment of $ 100000. It is likely to give $ 30000 every year over the next five years. The WACC of Christopher NATO is 12 %. So the NPV of the project is:

100000 – (30000 / ( 1 + .12) + 30000 / ( 1 + .12) ^ 2 + 30000 / (1 + .12) ^ 3 + 30000 / ( 1+.12) ^ 4 + 30000 / (1 + .12) ^ 5) = $ 8143.25.

The NPV of project A is positive. Therefore it can be concluded that project A will prove to be a profitable one for Christopher NATO limited.

The NPV method is the most complete method for capital projects’ appraisal. It is also the most widely used one because of its inherent merits. However the appraisal made by this technique can go off the mark if the future cash flows are not estimated rightly or if the WACC is not calculated accurately.

Internal Rate of Return Method:

The internal rate of return (IRR) is that discount rate at which the NPV of a project is zero. A project is profitable if the IRR is greater than the required rate of return of the company. The IRR is calculated usually by the hit-and-trial method. So suppose the required rate of return of Christopher NATO limited from investment in a project is 16 %. The IRR for a project A comes out to be 15 % while that of a competing project B is 17 %. Then Christopher NATO limited should accept project B and reject project A because B’s IRR is greater than the required rate of return while project A’s IRR is less than the required rate of return of Christopher NATO limited.

The IRR method suffers from certain shortcomings. If two competing projects have the same IRR then it will be impossible to choose between these projects using this method. The IRR method unlike the NPV doesn’t give the actual returns in absolute terms which the business will be likely to generate from investing in the project. This severely limits the utility of this method.

![]()

The IRR method is definitely inferior to the NPV method. The NPV method is therefore more widely used than IRR method. The right capital appraisal method leads the company to making right capital budgeting and investment decisions. A wrong appraisal method can lead the company to making loss making investment decisions. This will end up in the company destroying the wealth of its shareholders. Capital appraisal is therefore one of the most crucial activities of the finance division of most companies.

If you want Accounting Management Assignment Help study samples to help you write professional custom essay’s and essay writing help.

Receive assured help from our talented and expert writers! Did you buy assignment and assignment writing services from our experts in a very affordable price.

To get more information, please contact us or visit www.myassignmenthelp.Com